Compliance Alert | IRS Delay in 6055 and 6056 Reporting for 2018

Under the Patient Protection and Affordable Care Act (ACA), individuals are required to have health insurance, while applicable large employers (ALEs) are required to offer health benefits to their full-time employees. In order for the Internal Revenue Service (IRS) to verify that (1) individuals have the required minimum essential coverage, (2) individuals who request premium tax credits are entitled to them, and (3) ALEs are meeting their shared responsibility (play or pay) obligations, employers with 50 or more full-time or full-time equivalent employees and insurers are required to report on the health coverage they offer. The reporting requirements are in Sections 6055 and 6056 of the ACA.

Reporting was first due in 2016, based on coverage in 2015. Reporting in 2018 will be based on coverage in 2017. All reporting will be for the calendar year, even for non-calendar year plans.

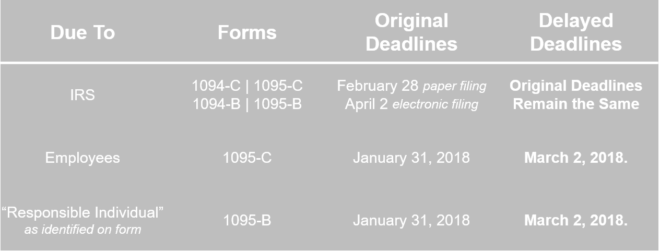

On December 22, 2017, the IRS issued Notice 2018-06, delaying the reporting deadlines in 2018 for the 1095-B and 1095-C forms to individuals. There is no delay for the 1094-C and 1094-B forms, or for forms due to the IRS.

Good Faith Effort

The IRS reiterated that, for the 2017 year reporting, relief is available to employers who make a good faith effort to comply with the information reporting requirements and they will not be subject to penalties for failure to correctly or completely file. This does not apply to employers that fail to timely file or furnish a statement. To determine if an employer made a “good faith effort,” the IRS will take into account whether an employer or other coverage provider made reasonable efforts to prepare for reporting the required information to the IRS and furnishing it to employees and covered individuals, such as gathering and transmitting the necessary data to an agent to prepare the data for submission to the IRS, or testing its ability to transmit information to the IRS. In addition, the IRS will also consider the extent to which the employer or other coverage provider is taking steps to ensure that it will be able to comply with the reporting requirements for 2018.

Extension Process

Generally, an automatic 30-day extension (for forms due to the IRS) will be given to entities by filing Form 8809, and no signature or explanation is needed. Form 8809 must be filed online or through the FIRE System, by the due date of returns in order to be granted the 30-day extension. Waivers may be requested with Form 8508, and are due at least 45 days before the due date of the information returns. This extension relates to the deadline to provide the IRS with the forms, not for providing individuals with the forms.

Because the transition relief outlined in Notice 2018-06 only relates to the forms for individuals, employers can still apply for extensions of time for filing returns to the IRS. Formal applications for extensions of time to provide individuals with forms will not receive responses because of the uniform extension given by Notice 2018-06.

Employers that have difficulty meeting the extended reporting deadlines are encouraged to file late, as the IRS will take late filing into consideration when determining whether to reduce or abate penalties for reasonable causes.

Impact on Individuals

The IRS has determined that individual taxpayers may be affected by the extension, as employees are not eligible for the premium tax credit for any month in which an employee is eligible for an employer plan that provides minimum value, affordable coverage.

Taxpayers may rely on other information received from employers about their offers of coverage for purposes of determining eligibility for the premium tax credit when filing their income tax returns and need not amend their returns once they receive their Form 1095-C or any corrected Form 1095-C. Individuals do not need to send this information to the IRS when filing their returns but should keep it with their tax records.

The extensions of due dates provided in the Notice apply only to Section 6055 and Section 6056 information returns and statements for the calendar year 2017 filed and furnished in 2018 and do not require the submission of any request or other documentation to the IRS.

1/2/2018