Compliance Recap | April 2018

April was a busy month in the employee benefits world.

April was a busy month in the employee benefits world.

The Internal Revenue Service (IRS) modified the 2018 health savings account (HSA) family contribution limit back to $6,900. The U.S. Department of Labor (DOL), U.S. Department of Health and Human Services (HHS), and the Treasury released proposed frequently asked questions regarding mental health parity.

The Centers for Medicare and Medicaid Services (CMS) released the 2019 parameters for the Medicare Part D prescription drug benefit, a 2019 Benefit and Payment Parameters final rule, a transitional policy extension for non-grandfathered coverage in the small group and individual health insurance markets, and an assignment schedule for new Medicare beneficiary identifiers.

The IRS released frequently asked questions on the employer credit for paid family medical leave. The Congressional Research Service (CRS) published a summary of federal requirements that apply to the private health insurance market.

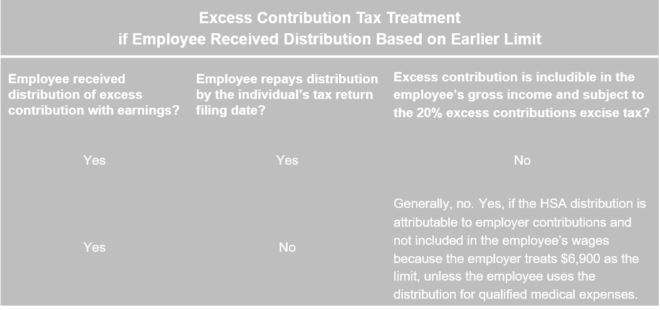

IRS Changes 2018 HSA Family Contribution Limit

The Internal Revenue Service (IRS) recently released Revenue Procedure 2018-27 to modify the 2018 health savings account (HSA) family contribution limit back to $6,900. This is the second, and likely final, change in limit during 2018.

As background, in May 2017, the IRS released Revenue Procedure 2017-37 that set the 2018 HSA family contribution limit at $6,900.

However, in March 2018, the IRS released Revenue Procedure 2018-10 that adjusted the annual inflation factor for some tax-related formulas from the Consumer Price Index (CPI) to a new factor called a “chained CPI.” As a result, the 2018 HSA family contribution limit was lowered to $6,850 from $6,900, retroactively effective to January 1, 2018.

Stakeholders informed the IRS that the lower HSA contribution limit would impose many unanticipated administrative and financial burdens. In response and in the best interest of sound and efficient tax administration, the IRS will allow taxpayers to treat the originally published $6,900 limit as the 2018 HSA family contribution limit.

DOL, HHS, and Treasury Release Proposed FAQs on Mental Health Parity

The U.S. Departments of Labor (DOL), Health and Human Services (HHS), and the Treasury (collectively, the “Departments”) released proposed FAQs About Mental Health and Substance Use Disorder Parity Implementation and the 21st Century Cures Act Part XX.

The Departments respond to FAQs as part of implementing the Paul Wellstone and Pete Domenici Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA).

Generally, the MHPAEA requires that the financial requirements (for example, coinsurance and copays) and treatment limitations (for example, visit limits) imposed on mental health or substance abuse disorder (MH/SUD) benefits cannot be more restrictive than the predominant financial requirements and treatment limitations that apply to substantially all medical/surgical benefits in a class.

Similarly, a group health plan or issuer cannot impose a nonquantitative treatment limitation (NQTL) on MH/SUD benefits that are more stringent than a comparable limitation that is applied to medical/surgical benefits.

The MHPAEA regulations include express disclosure requirements. For example, if a participant requests the criteria for medical necessity determinations regarding MH/SUD benefits, then the plan administrator must make the information available to the participant.

To assist plan sponsors with disclosure requests, DOL released a revised draft Mental Health and Substance Use Disorder Parity Disclosure Request that plan sponsors may provide to individuals who request information from an employer-sponsored health plan regarding treatment limitations.

To assist plan sponsors in determining whether a group health plan complies with MHPAEA, the DOL released its Self-Compliance Tool for the Mental Health Parity and Addiction Equity Act.

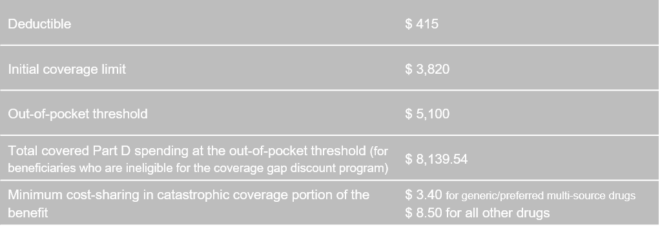

CMS Releases 2019 Parameters for Medicare Part D Prescription Drug Benefit

The Centers for Medicare and Medicaid Services (CMS) released the following parameters for the defined standard Medicare Part D prescription drug benefit for 2019:

Generally, group health plan sponsors must disclose to Part D eligibility individuals whether the prescription drug coverage offered by the employer is creditable. Coverage is creditable if it, on average, pays out at least as much as coverage available through the defined standard Medicare Part D prescription drug plan.

CMS Issues 2019 Benefit and Payment Parameters Final Rule

The Centers for Medicare and Medicaid Services (CMS) published its 2019 Benefit and Payment Parameters final rule. The rule primarily affects the individual health insurance market inside and outside of the Exchange, the small group health insurance market, issuers, and the states.

Within the rule, three items most directly affect employers and their group health plans:

- Maximum annual out-of-pocket limit on cost sharing for 2019

- New methods for changing state EHB-benchmark plans

- New requirements for employers and issuers participating in the Small Business Health Options Program (SHOP) Marketplace

Read more about the final rule.

CMS Issues Transitional Policy Extension

The Centers for Medicare and Medicaid Services (CMS) issued a bulletin extending its transitional policy.

As background, in November 2013, CMS announced a transitional policy for non-grandfathered coverage in the small group and individual health insurance markets. Under its policy, health insurance issuers may choose to continue certain coverage that would otherwise be canceled because of noncompliance with Patient Protection and Affordable Care Act (ACA) and Public Health Service Act (PHS Act). Further, affected small businesses and individuals may choose to re-enroll in such coverage.

Under its policy, non-grandfathered health insurance coverage in the small group and individual health insurance markets will not be considered to be out of compliance with the following ACA and PHS Act market reforms if certain criteria are met:

- Fair health insurance premiums

- Guaranteed availability of coverage

- Guaranteed renewability of coverage

- Prohibition of pre-existing condition exclusions or other discrimination based on health status, with respect to adults, except with respect to group coverage

- Prohibition of discrimination against individual participants and beneficiaries based on health status, except with respect to group coverage

- Non-discrimination in health care

- Coverage for individuals participating in approved clinical trials

- Single risk pool requirement

Under CMS’ transitional policy, states may permit issuers that have renewed policies under the transitional policy continually since 2014 to renew such coverage for a policy year starting on or before October 1, 2019. However, any policies renewed under this transitional policy must not extend past December 31, 2019.

CMS Starts Assigning New Medicare Beneficiary Identifiers

The Centers for Medicare and Medicaid Services (CMS) started issuing new Medicare cards with a Medicare Beneficiary Identifier (MBI) or Medicare number. The MBI will replace the Social Security number-based Health Insurance Claim Number (HICN) for Medicare transactions such as billing, eligibility status, and claim status.

New enrollees will be among the first to get these new cards. Current Medicare beneficiaries will get their new cards on a rolling basis over the next few months.

Employers who are currently capturing the HICN for their active employee or retirees should update their systems to accept the new MBIs.

IRS Releases FAQ on Employer Credit for Paid Family Medical Leave

The IRS released an FAQ that primarily reiterates the Tax Cuts and Jobs Act’s provisions that provide a new federal credit for employers that provide paid family and medical leave to their employees.

The IRS explains that an employer must reduce its deduction for wages or salaries paid or incurred by the amount determined as a credit. Also, any wages taken into account in determining any other general business credit may not be used in determining this credit.

The IRS adds this definition of “paid family and medical leave” that, for purposes of the credit, includes time off for:

- Birth of an employee’s child and to care for the child.

- Placement of a child with the employee for adoption or foster care

- To care for the employee’s spouse, child, or parent who has a serious health condition

- A serious health condition that makes the employee unable to perform the functions of his or her position

- Any qualifying exigency due to an employee’s spouse, child, or parent being on covered active duty (or having been notified of an impending call or order to covered active duty) in the Armed Forces.

- To care for a service member who is the employee’s spouse, child, parent, or next of kin

The FAQ also explains that, in the future, the IRS intends to address:

- When the written policy must be in place

- How paid “family and medical leave” relates to an employer’s other paid leave

- How to determine whether an employee has been employed for “one year or more”

- The impact of state and local leave requirements

- Whether members of a controlled group of corporations and businesses under common control are treated as a single taxpayer in determining the credit

Read more about the federal tax credit for employer-provided paid family and medical leave.

CRS Publishes Federal Requirements on Private Health Insurance Plans

The Congressional Research Service (CRS) published Federal Requirements on Private Health Insurance Plans, which summarizes federal requirements that apply to the private health insurance market, including a table that indicates whether a particular federal requirement applies to a fully-insured large group plan, fully-insured small group plan, self-funded plan, or individual coverage.

The Question of the Month

- What are the penalties for failing to comply with Section 125 requirements, such as failing to follow a cafeteria plan document’s terms?

- An operational failure occurs when a plan fails to follow its cafeteria plan document’s terms. There are several potential penalties for operational failures, including:

- Cafeteria plan disqualification

- Requiring the cafeteria plan to comply with Section 125 and its regulations, including reversing transactions that caused noncompliance

- Imposing employment tax withholding liability and penalties on the employer regarding pre-tax salary reductions and elective employer contributions

- Imposing employment and income tax liability and penalties on employees regarding pre-tax salary reductions and elective employer contributions