Compliance Recap | January 2021

January was a busy month in the employee benefits world.

President Biden issued a memorandum putting a regulatory freeze on new rules. President Biden also issued an executive order on strengthening Medicaid and the Patient Protection and Affordable Care Act (ACA).

The Department of Labor (DOL) released inflation-adjusted federal civil penalty amounts. The Centers for Medicare and Medicaid Services (CMS) issued its parameters for the defined standard Medicare Part D prescription drug benefit for 2022.

The Internal Revenue Service (IRS) released final rules on individual coverage health reimbursement arrangements (ICHRAs). Former President Trump signed an amendment to the Health Information Technology for Economic and Clinical Health Act (HITECH Act) that requires the Department of Health and Human Services (HHS) to consider recognized security practices that a covered entity or business associate had in place for purposes of HHS determining penalties and audit outcomes.

HHS extended the transitional relief from certain health care reform requirements for grandmothered plans. CMS released the final 2022 benefit payment and parameters rule.

The Equal Employment Opportunity Commission (EEOC) released unofficial proposed rules on wellness programs subject to the Americans with Disabilities Act of 1990 (ADA) or Genetic Information Nondiscrimination Act of 2008 (GINA). The IRS released the 2020 Publication 502 – Medical and Dental Expenses for use in preparing 2020 tax returns. The EEOC also issued an opinion letter on ICHRAs and age discrimination.

Former President Trump signed the Competitive Health Insurance Reform Act of 2020 that limits the antitrust exemption that is available to health insurance companies. The DOL rescinded the rule on promoting regulatory openness through good guidance.

The employee retention tax credit extension under the Taxpayer Certainty and Disaster Tax Relief Act of 2020 became effective.

President Biden Issues Regulatory Freeze Pending Review

On January 20, 2021, President Biden issued a Memorandum for the Heads of the Executive Departments and Agencies (Memorandum). The Memorandum instructs the executive departments and federal agencies to refrain from proposing or issuing a rule until a department or agency head that has been appointed by President Biden has reviewed and approved the rule. The memorandum further instructs the executive departments and agencies to withdraw rules that have been sent to the Federal Register, but not yet published, and to consider delaying implementation of rules that have been published until they can be reviewed and approved by a department or agency head that has been appointed by President Biden.

President Biden Issues Executive Order on Strengthening Medicaid and the ACA

On January 28, 2021, President Biden signed an Executive Order on Strengthening Medicaid and the Affordable Care Act (ACA) (Executive Order). The Executive Order instructs HHS to consider establishing a special open enrollment period (SEP) for individuals to enroll in or change their current coverage under federally facilitated health insurance marketplaces. CMS has established that the special enrollment period will begin on February 15, 2021, and will continue through May 15, 2021. The Executive Order also instructs HHS, DOL, the Treasury, and all other executive departments and agencies with authorities and responsibilities related to Medicaid and the ACA to review existing regulations and other guidance and determine whether to suspend, revise, or revoke such regulations and guidance.

Read more about the Executive Order.

DOL Releases Inflation-Adjusted Federal Civil Penalty Amounts

On January 14, 2021, the DOL issued its Federal Civil Penalties Inflation Adjustment Act Annual Adjustments for 2021 which is the DOL’s annual adjustment of federal civil monetary penalties.

Here are some of the adjustments:

- Form 5500: For failure to file, the maximum penalty increases from $2,233 to $2,259 daily for every day that the Form 5500 is late.

- Summary of Benefits and Coverage: For failure to provide, the maximum penalty increases from $1,176 to $1,190 per failure.

- Medicaid/CHIP notice: For failure to provide, the maximum penalty increases from $119 to $120 per day per employee.

- For failure to provide documents to the DOL upon its request, the maximum penalty increases to $161 per day, not to exceed $1,613 per request.

The adjustments are effective for penalties assessed after January 15, 2021, for violations occurring after November 2, 2015.

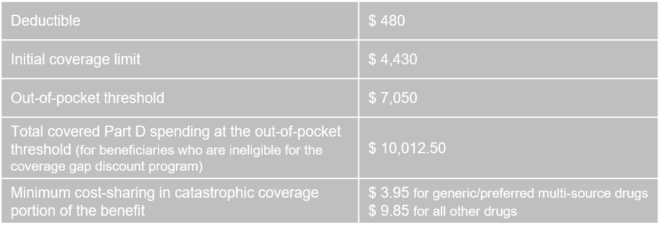

CMS Releases 2022 Parameters for Medicare Part D Prescription Drug Benefit

CMS released the following parameters for the defined standard Medicare Part D prescription drug benefit for 2022:

Generally, group health plan sponsors must disclose to Part D eligible individuals whether the prescription drug coverage offered by the employer is creditable. Coverage is creditable if, on average, it pays out at least as much as coverage available through the defined standard Medicare Part D prescription drug plan.

IRS Releases Final Rules on ICHRAs

The IRS released final rules clarifying how the employer shared responsibility provisions and Section 105(h) nondiscrimination rules apply to ICHRAs that are integrated with individual health insurance coverage or Medicare. The final rules provide minor clarifications to the proposed rules. The final rules are scheduled to take effect once they are filed in the Federal Register.

Read more about the final rules on ICHRAs.

Former President Trump Signed HITECH Act Amendment

On January 5, 2021, former President Trump signed an amendment to the HITECH Act that requires HHS to consider “recognized security practices” that a covered entity or business associate has had in place for at least 12 months for purposes of HHS determining 1) whether and to what extent fines should be levied against covered entities or business associations; 2) the outcome of an audit; and 3) the remedies that a covered entity or business associate must agree to when resolving potential violations of the Health Insurance Portability and Accountability Act of 1996 (HIPAA) Security Rule with HHS.

Under the amendment, recognized security practices include the standards, guidelines, best practices, methodologies, procedures, and processes developed under the National Institute of Standards and Technology Act, approaches set forth under the Cybersecurity Act of 2015, and other programs and processes that address cybersecurity set forth in regulations under other laws.

HHS Extends Transitional Relief for Grandmothered Plans

As background, in the fall of 2013, HHS announced a transitional relief program that allowed state insurance departments to permit early renewal at the end of 2013 of individual and small group policies that do not meet the “market reform” requirements of the ACA and for the policies to remain in force until their new renewal date in late 2014.

The transitional relief has been extended multiple times, including the latest extension under an HHS bulletin to permit renewals on or before October 1, 2022, provided that the coverage comes into compliance with the market reform requirements by January 1, 2023. However, states may prohibit the renewal of these plans.

CMS Releases the Final 2022 Benefit Payment and Parameters Rule

CMS has released a final rule along with a fact sheet and press release for benefit payment and parameters for 2022.

According to CMS, the proposed 2022 benefit payment and parameters rule intended to reduce fiscal and regulatory burdens associated with the ACA across different program areas and to provide stakeholders with greater flexibility. The final rule addresses only a subset of the proposed provisions contained in the proposed rule. See our Advisor on the proposed rule.

The final rule primarily affects the individual market and the Exchanges. However, the final rule includes a provision regarding premium payments from ICHRAs and qualified small employer health reimbursement arrangements (QSEHRAs) that are made to issuers of individual health plans.

The final rule is scheduled to take effect on March 15, 2021.

Read more about the final rule.

EEOC Releases Unofficial Proposed Rules on Wellness Programs Subject to the ADA or GINA

The EEOC released unofficial proposed rules for wellness programs subject to the Americans with Disabilities Act (ADA) and for wellness programs subject to the Genetic Information Nondiscrimination Act (GINA). The proposed rules would amend the current ADA and GINA wellness program rules, with the most anticipated change being the proposed establishment of the level of incentive (or penalty) that employers may provide under wellness programs.

Read more about the proposed rules.

IRS Releases 2020 Publication 502 – Medical and Dental Expenses

The Internal Revenue Service (IRS) released 2020 Publication 502 – Medical and Dental Expenses for use in preparing 2020 tax returns.

EEOC Opinion Letter on ICHRAs

The EEOC released an opinion letter in response to an inquiry regarding whether two ICHRA plan designs would violate the Age Discrimination in Employment Act of 1967 (ADEA). Under the first design, the employer contributes the same dollar amount for all participating employees’ ICHRAs even though older employees will have to pay higher insurance premiums on the individual market. In the EEOC’s opinion, the design does not violate the ADEA because the same contribution amount is provided to all participants regardless of age and because employees do not contribute to ICHRAs they are not subject to the ADEA’s prohibition against requiring older workers to bear a greater proportion of the cost of a fringe benefit than younger workers.

Under the second design, the employer contributes a set percentage (for example 30 percent) of the individual health insurance premium for all participating employees’ ICHRAs, meaning older employees will receive a higher ICHRA contribution because they will have to pay higher insurance premiums on the individual market. In the EEOC’s opinion, providing larger contribution amounts to older participant’s ICHRAs does not violate the ADEA. Furthermore, because the regulations governing ICHRAs do not permit employers to decrease ICHRA contributions as a participant’s age increases, the EEOC provides that ICHRAs that comply with the current tri-agency regulations on ICHRAs will not violate the ADEA’s prohibition against providing decreased compensation based on age.

Former President Trump Signed the Competitive Health Insurance Reform Act of 2020

On January 13, 2021, former President Trump signed the Competitive Health Insurance Reform Act of 2020 (Act). The Act limits the antitrust exemption that is available to health insurance companies under federal antitrust laws. Under the Act, health insurers are subject to the federal antitrust laws except for certain activities that improve health insurance services for consumers.

DOL Rescinds Rule on Promoting Regulatory Openness Through Good Guidance

As background, in 2020 the DOL released a final rule on Promoting Regulatory Openness Through Good Guidance (PRO Good Guidance) and a fact sheet. The PRO Good Guidance rule communicated the DOL’s policies for issuing, modifying, withdrawing, applying guidance, making guidance available to the public, notice-and-comment procedures for significant guidance, and responding to petitions from the public about guidance.

On January 25, 2021, the DOL rescinded this rule in response to President Biden’s executive order directing agencies to rescind rules and guidance published under the Trump Administration in order to give agencies flexibility in determining when and how to best issue public guidance.

Extension of the Employee Retention Tax Credit

The Taxpayer Certainty and Disaster Tax Relief Act of 2020, enacted December 27, 2020, extended the Employee Retention Tax Credit (“credit”) that was established by the CARES Act, to the first two quarters in 2021. Effective January 1, 2021, the credit will be available to businesses with operations that are either fully or partially suspended by a COVID-19 governmental order and only during the period in which the order is in force, or if gross receipts are less than 80 percent of gross receipts for the same quarter in 2019. In addition, the new rule allows an employer to elect to use the gross receipts from the immediately preceding quarter, and compare these prior quarter gross receipts to the same quarter in 2019, rather than the current quarter.

Beginning January 1, 2021, the credit is 70 percent of qualified wages up to $10,000 per quarter for each employee. Accordingly, the cap is $7,000 per employee for each of the first two quarters of 2021 ($10,000 in qualified wages x 70%) for a possible $14,000 credit per employee. This year, a company with more than 500 employees cannot take the credit for wages paid to an employee performing services for the employer (either teleworking, or working at the workplace, even though at reduced capacity due to reduction in business). An employer with 500 or fewer employees will be eligible for the credit, even if employees are working. The 500-employee threshold was increased from the 100 employee threshold under the CARES Act.

Question of the Month

- When a group health plan changes, when should I generally give notice to participants?

- Depending on the change that is made, an employer must provide notice within one of three time frames:

- 60 days prior to the change

- No later than 60 days after the change (or, within 60 days of the change)

- Within 210 days after the end of the plan year

For modifications to the summary plan description (SPD) that constitute a material reduction in covered services or benefits, notice is required within 60 days of adoption of the material reduction in group health plan services or benefits. For example, a decrease in employer contribution would be a material reduction in covered services or benefits so notice should be provided within 60 days of the change in employer contribution. As a best practice, an employer should give advance notice of the change. For practical purposes, employees should be told prior to the first increased withholding.

If a plan makes a material modification in any of the plan terms that would affect the content of the most recently provided summary of benefits and coverage (SBC), then notice must be provided no later than 60 days prior to the date on which the modification will become effective.

However, if the change is part of open enrollment, assuming you communicate the change during open enrollment, the open enrollment communication is considered acceptable notice, regardless of whether the SBC or the SPD, or both, are changing. Open enrollment is essentially a safe harbor for the 60-day prior/60-day post notice requirements.

Finally, changes that do not require more immediate notifications, because they do not affect the SBC and are not a material reduction in benefits, must be communicated through a summary of material modifications or an updated summary plan description within 210 days after the end of the plan year. Note, a group health plan may be able to extend the deadlines noted above due to COVID-19 under EBSA Disaster Relief Notice 2020-01 and HHS, DOL, and the Treasury FAQs Part 43.

2/1/2021