Compliance Recap | November 2018

November was a busy month in the employee benefits world.

The Internal Revenue Service (IRS) extended the due date for employers to furnish Forms 1095-C or 1095-B to individuals, extended “good faith compliance efforts” relief for 2018, and issued specifications for employer-provided substitute ACA forms. The Department of the Treasury (Treasury), Department of Labor (DOL), and Department of Health and Human Services (HHS) released two final rules on contraceptive coverage exemptions.

The IRS released indexed Patient-Centered Outcomes Research Institute (PCORI) fees and inflation-adjusted limits for various benefits. The DOL, IRS, and the Pension Benefit Guaranty Corporation (PBGC) released advance informational copies of the 2018 Form 5500 annual return/report and instructions.

For survivors of the 2018 California wildfires, the IRS provided tax relief and the DOL released employee benefit guidance. The IRS provided guidance to employers who adopt leave-based donation programs to provide charitable relief for victims of Hurricane Michael. The Treasury released its Priority Guidance Plan that lists projects that will be the focus of the Treasury and IRS for the period from July 1, 2018, through June 30, 2019.

IRS Extends Due Date to Furnish ACA Forms to Participants and Provides Good Faith Penalty Relief

The Internal Revenue Service (IRS) issued Notice 2018-94 to extend the due date to furnish 2018 Forms 1095-B and 1095-C to individuals. The due date moves from January 31, 2019, to March 4, 2019.

The IRS also extends “good faith compliance efforts” relief for 2018. As in prior years, this relief is applied only to incorrect or incomplete information reported in good faith on a statement or return. The relief does not apply to a failure to timely furnish a statement or file a return.

IRS Issues Specifications for Employer-Provided Substitute ACA Forms

The Internal Revenue Service (IRS) issued Publication 5223 General Rules and Specifications for Affordable Care Act Substitute Forms 1095-A, 1094-B, 1095-B, 1094-C, and 1095-C that describes how employers may prepare substitute forms to furnish ACA reporting information to individuals and the IRS.

Treasury, DOL, and HHS Release Two Final Rules on Contraceptive Coverage Exemptions

The Department of the Treasury (Treasury), Department of Labor (DOL), and Department of Health and Human Services (HHS) (collectively, Departments) released two final rules on contraceptive coverage exemptions. These rules finalize the Departments’ interim final rules that were published on October 13, 2017. HHS also issued a press release and fact sheet on these final rules.

The first final rule provides an exemption from the contraceptive coverage mandate to entities (including certain employers) and individuals that object to services covered by the mandate on the basis of sincerely held religious beliefs.

The second final rule provides an exemption from the contraceptive coverage mandate to nonprofit organizations, small businesses, and individuals that object to services covered by the mandate on the basis of sincerely held moral convictions.

The final rules will be effective on January 14, 2019.

IRS Releases Indexed PCORI Fee

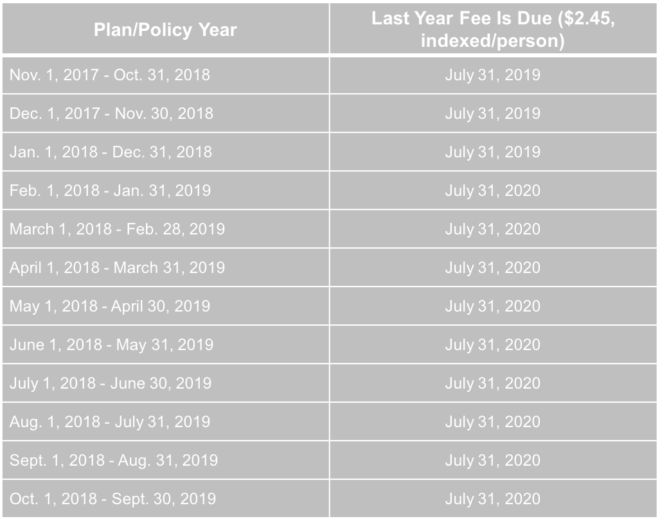

The Patient Protection and Affordable Care Act (ACA) imposes a fee on insurers of certain fully insured plans and plan sponsors of certain self-funded plans to help fund the Patient-Centered Outcomes Research Institute (PCORI). The PCORI fee is due by July 31 of the year following the calendar year in which the plan or policy year ends.

The Internal Revenue Service issued Notice 2018-85 to announce the PCORI fee of $2.45 for policy years and plan years that end on or after October 1, 2018, and before October 1, 2019.

IRS Releases 2019 Inflation-Adjusted Limits

The Internal Revenue Service (IRS) released its inflation-adjusted limits for various benefits. For example, the maximum contribution limit to health flexible spending arrangements (FSAs) will be $2,700 in 2019. Also, the maximum reimbursement limit in 2019 for Qualified Small Employer Health Reimbursement Arrangements will be $5,150 for single coverage and $10,450 for family coverage.

Advance Informational Copies of 2018 Form 5500 Annual Return/Report

The U.S. Department of Labor’s Employee Benefits Security Administration (EBSA), the Internal Revenue Service (IRS), and the Pension Benefit Guaranty Corporation (PBGC) released advance informational copies of the 2018 Form 5500 annual return/report and related instructions.

Here are some of the changes that the instructions highlight:

- Principal Business Activity Codes.Principal Business Activity Codes have been updated to reflect updates to the North American Industry Classification System (NAICS). For Line 2d, a plan administrator would enter the six-digit Principal Business Activity Code that best describes the nature of the plan sponsor’s business from the list of codes on pages 78-80 of the Form 5500 Instructions.

- Administrative Penalties. The instructions have been updated to reflect that the new maximum penalty for a plan administrator who fails or refuses to file a complete or accurate Form 5500 report has been increased to up to $2,140 a day for penalties assessed after January 2, 2018, whose associated violations occurred after November 2, 2015.

Because the Federal Civil Penalties Inflation Adjustment Improvements Act of 2015 requires the penalty amount to be adjusted annually after the Form 5500 and its schedules, attachments, and instructions are published for filing, be sure to check for any possible required inflation adjustments of the maximum penalty amount that are published in the Federal Register after the instructions have been posted.

- Form 5500-Participant Count.The instructions for Lines 5 and 6 have been enhanced to make clearer that welfare plans complete only Line 5 and elements 6a(1), 6a(2), 6b, 6c, and 6d in Line 6.

Be aware that the advance copies of the 2018 Form 5500 are for informational purposes only and cannot be used to file a 2018 Form 5500 annual return/report.

ERISA imposes the Form 5500 reporting obligation on the plan administrator. Form 5500 is normally due on the last day of the seventh month after the close of the plan year. For example, a plan administrator would file Form 5500 by July 31, 2019, for a 2018 calendar year plan.

Tax Relief for Victims of November Wildfire in California

Victims of the wildfires that took place beginning on November 8, 2018, in California may qualify for tax relief from the Internal Revenue Service (IRS). The President declared that a major disaster exists in California. The Federal Emergency Management Agency’s major declaration permits the IRS to postpone deadlines for taxpayers who have a business in certain counties within the disaster area.

The IRS automatically identifies taxpayers located in the covered disaster area and applies automatic filing and payment relief. But affected taxpayers who reside or have a business located outside the covered disaster area must call the IRS disaster hotline at 866-562-5227 to request this tax relief.

DOL Releases Employee Benefit Guidance and Relief for 2018 California Wildfire Survivors

The Department of Labor (DOL) released its FAQs for Participants and Beneficiaries Following the 2018 California Wildfires to answer health benefit and retirement benefit questions.

The FAQs cover topics including:

- Whether an employee will still be covered by an employer-sponsored group health plan if the worksite closed

- Potential options such as special enrollment rights, COBRA continuation coverage, individual health coverage, and health coverage through a government program in the event that an employee loses health coverage

The DOL also released its Fact Sheet: Guidance and Relief for Employee Benefit Plans Impacted by the 2018 California Wildfires to recognize that employers may encounter problems due to the wildfires. The DOL advises plan fiduciaries to make reasonable accommodations to prevent workers’ loss of benefits and to take steps to minimize the possibility of individuals losing benefits because of a failure to comply with pre-established time frames.

The DOL also acknowledged that there may be instances when full and timely compliance by group health plans may not be possible due to physical disruption to a plan’s principal place of business. The DOL’s enforcement approach will emphasize compliance assistance, including grace periods and other relief where appropriate.

IRS Provides Guidance on Leave-Based Donation Programs’ Tax Treatment

The IRS issued Notice 2018-89 to guide employers who adopt leave-based donation programs to provide charitable relief for victims of Hurricane Michael. These leave-based donation programs allow employees to forgo vacation, sick, or personal leave in exchange for cash payments that the employer will make to charitable organizations described under Internal Revenue Code Section 170(c).

The employer’s cash payments will not constitute gross income or wages of the employees if paid before January 1, 2020, to the Section 170(c) charitable organizations for the relief of victims of Hurricane Michael. Employers do not need to include these payments in Box 1, 3, or 5 of an employee’s Form W-2.

Treasury Releases 2018-19 Priority Guidance Plan

The Department of the Treasury (Treasury) released its 2018-2019 Priority Guidance Plan (Plan) that describes the priorities for the Treasury and the Internal Revenue Service (IRS) for the period from July 1, 2018, through June 30, 2019. The Plan contains a list of projects that will be the focus of the Treasury and IRS, including:

- Guidance on employer shared responsibility provisions

- Regulations regarding the excise tax on high cost employer-provided coverage (also known as the “Cadillac tax”).

Question of the Month

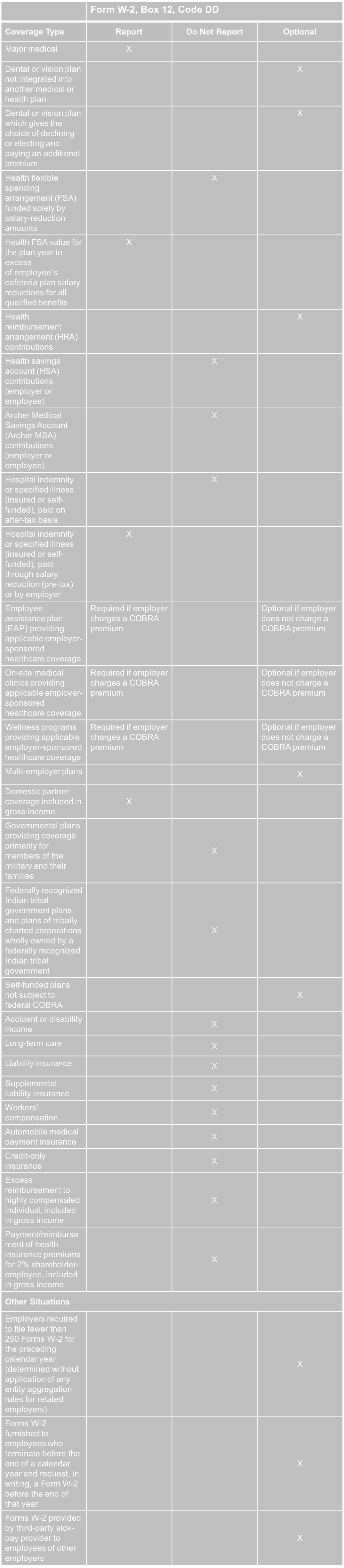

- Under the ACA, which employers must report information on Form W-2 and what information must be reported?

- The ACA requires employers to report the cost of coverage under an employer-sponsored group health plan. Reporting the cost of health care coverage on Form W-2 does not mean that the coverage is taxable.

Employers that provide “applicable employer-sponsored coverage” under a group health plan are subject to the reporting requirement. This includes businesses, tax-exempt organizations, and federal, state and local government entities (except with respect to plans maintained primarily for members of the military and their families). Federally recognized Indian tribal governments are not subject to this requirement.

Employers that are subject to this requirement should report the value of the health care coverage in Box 12 of Form W-2, with Code DD to identify the amount. There is no reporting on Form W-3 of the total of these amounts for all the employer’s employees.

In general, the amount reported should include both the portion paid by the employer and the portion paid by the employee. Please see the chart below from the IRS’ webpage and its questions and answers for more information.

The chart below illustrates the types of coverage that employers must report on Form W-2. Certain items are listed as “optional” based on transition relief provided by Notice 2012-9 (restating and clarifying Notice 2011-28). Future guidance may revise reporting requirements but will not be applicable until the tax year beginning at least six months after the date that the IRS issues its guidance.

Form W-2 Reporting of Employer-Sponsored Health Coverage