Compliance Recap | November 2019

November was a busy month in the employee benefits world.

The Internal Revenue Service (IRS) released draft 2019 instructions for Forms 1094-B, 1095-B, 1094-C, and 1095-C. The IRS also released health plan limits and various compensation, benefit, and contribution levels under qualified retirement plans for 2020.

The Department of Health and Human Services (HHS) released inflation-adjusted civil monetary penalty amounts. The Department of Labor (DOL) released advance copies of Form 5500 and related instructions for 2019.

The Centers for Medicare and Medicaid Services (CMS) released Summary of Benefits and Coverage (SBC) materials and supporting documents for plan years beginning 2021. A district court vacated the conscience rights protection final rule. The IRS, DOL, and HHS (collectively, Departments) released proposed rules on coverage transparency for health plans and issuers and final rules on price transparency requirements for hospitals.

IRS Releases Draft 2019 Instructions for Forms 1094-B, 1095-B, 1094-C, and 1095-C

The IRS released draft instructions for both the 1094-B and 1095-B forms and the 1094-C and 1095-C forms and the draft forms for 1094-B, 1095-B, 1094-C, and 1095-C. There are no substantive changes in the forms or instructions between 2018 and 2019. The IRS notes in the Form 1095-B instructions that the individual shared responsibility penalty has been reduced to $0 for an individual who does not have minimum essential coverage.

Read more about the draft forms and instructions.

IRS Releases 2020 Inflation-Adjusted Limits

The Internal Revenue Service (IRS) released health plan limits, such as the health flexible spending arrangement (FSA) contribution limit of $2,750, as well as various compensation, benefit, and contribution levels under qualified retirement plans for 2020.

Download a summary of the 2020 annual benefit plan limits.

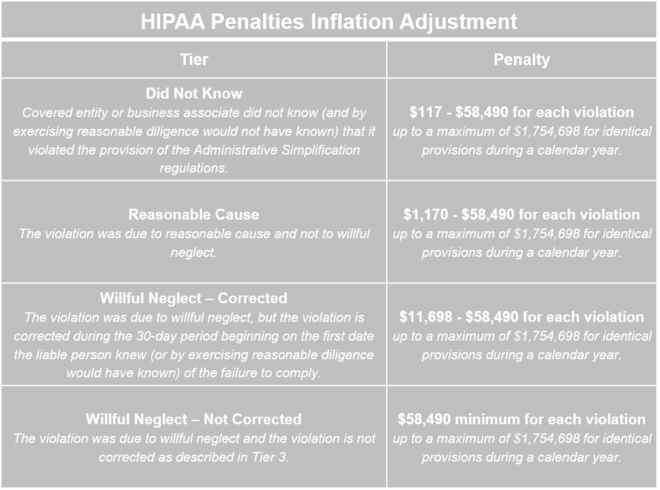

HHS Releases Inflation-Adjusted Federal Civil Penalty Amounts

The Department of Health and Human Services (HHS) issued its Annual Civil Monetary Penalties Inflation Adjustment. Here are some of the adjustments:

- Medicare Secondary Payer:

- For failure to provide information identifying situations where the group health plan is primary, the maximum penalty increases from $1,181 to $1,211 per failure.

- For an employer who offers incentives to a Medicare-eligible individual to not enroll in an employer-sponsored group health plan that would otherwise be primary, the maximum penalty increases from $9,239 to $9,472.

- For willful or repeated failure to provide requested information regarding group health plan coverage, the maximum penalty increases from $1,504 to $1,542.

- Summary of Benefits and Coverage: For failure to provide, the maximum penalty increases from $1,128 to $1,156 per failure.

- Health Insurance Portability and Accountability Act (HIPAA):

The adjustments are effective for penalties assessed on or after November 5, 2019, for violations occurring after November 2, 2015.

DOL Releases Advance Copies of Form 5500 and Related Instructions for 2019

The Department of Labor (DOL) released advance copies of Form 5500 Annual Return / Report (Form 5500) and related instructions for 2019. The advance copies of the 2019 Form 5500 are for informational purposes only and cannot be used to file a 2019 Form 5500.

CMS Releases SBC Materials for Plan Years Beginning 2021

The Centers for Medicare and Medicaid Services (CMS) released SBC materials and supporting documents including a template SBC, sample completed SBC, uniform glossary, instructions, and guidance for plan or policy years beginning on or after January 1, 2021.

District Court Vacates Conscience Rights Protection Final Rule

As background, on May 21, 2019, the Department of Health and Human Services (HHS) published a final rule and released a fact sheet to implement the conscience rights protection provisions contained in federal laws such as the Church Amendments, the Coats-Snowe Amendment, the Weldon Amendment, and the Patient Protection and Affordable Care Act (ACA).

The final rule stated that it did not create any new conscience rights protection. Individuals, health care entities (including health plans and plan sponsors), and providers are protected from discrimination in health care (based on their religious belief or moral conviction) by government or government-funded entities. The final rule requires applicants for and recipients of federal financial assistance from HHS to attest that they will comply with conscience rights and anti-discrimination laws. The final rule implemented enforcement tools, such as investigating complaints, compliance reviews, and withholding federal funds, similar to other civil rights laws, to ensure compliance with federal conscience rights protection laws.

On November 6, 2019, the U.S. District Court for the Southern District of New York (district court) vacated the entire final rule on a nationwide basis. The case consolidated three lawsuits challenging the final rule led by the State of New York, the National Family Planning and Reproductive Health Association, and Planned Parenthood. The district court found that despite HHS’ characterization of the final rule as merely a housekeeping rule that implements preexisting conscience protections enacted by Congress, the final rule is a substantive rule that creates new obligations and penalties. The court held that HHS did not have the authority to issue substantive rules regarding federal conscience protection provisions contained in the Church, Coats-Snowe, and Weldon Amendments.

IRS, DOL, and HHS Issue Proposed Rules on Coverage Transparency and Final Rules on Hospital Price Transparency

On November 15, 2019, the Internal Revenue Service (IRS), Department of Labor (DOL), and the Department of Health and Human Services (HHS) (collectively, Departments) released proposed rules on coverage transparency and final rules on price transparency requirements for hospitals. HHS issued a press release regarding the proposed rules and the final rules.

The proposed rules would require group health plans and insurance issuers in the individual and group markets to disclose cost-sharing information and negotiated rates. The proposed rules would also allow issuers that encourage participants to shop for lower cost services to take credit for “shared savings” payments they provide to participants in their medical loss ratio (MLR) calculations. HHS released a fact sheet regarding the proposed rules.

The final rules establish requirements for hospitals to create, update, and make public a list of their standard charges, including payer-specific negotiated charges, for the items and services they provide. HHS released a fact sheet regarding the final rules.

The final rules on hospital price transparency are effective on January 1, 2021.

Read more about the proposed and final rules.

Question of the Month

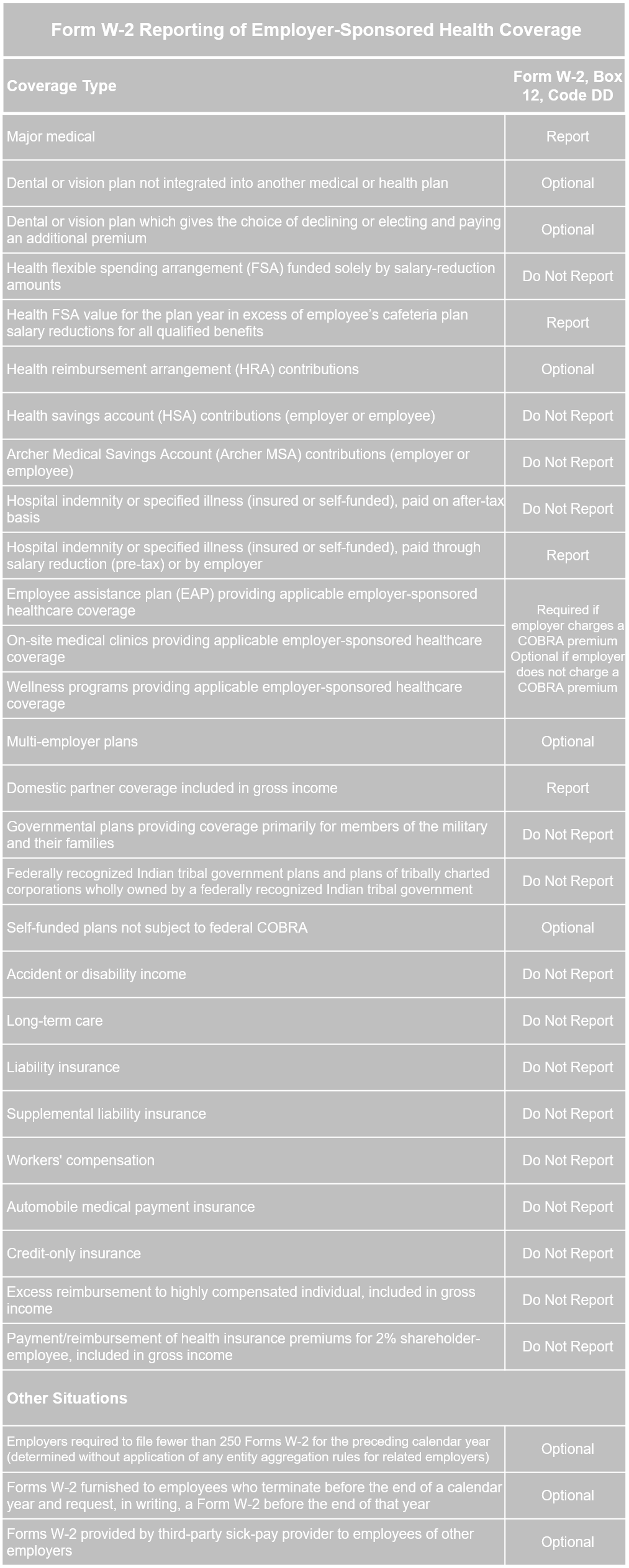

- Under the ACA, which employers must report information on Form W-2 and what information must be reported?

- The ACA requires employers to report the cost of coverage under an employer-sponsored group health plan. Reporting the cost of health care coverage on Form W-2 does not mean that the coverage is taxable.

Employers that provide “applicable employer-sponsored coverage” under a group health plan are subject to the reporting requirement. This includes businesses, tax-exempt organizations, and federal, state and local government entities (except with respect to plans maintained primarily for members of the military and their families). Federally recognized Indian tribal governments are not subject to this requirement.

Further, under transition relief provided by Notice 2012-9, an employer is not required to report the cost of coverage on Form W-2 if the employer filed fewer than 250 Forms W-2 for the previous calendar year.

Employers that are subject to this requirement should report the value of the health care coverage in Box 12 of Form W-2, with Code DD to identify the amount. There is no reporting on Form W-3 of the total of these amounts for all the employer’s employees.

In general, the amount reported should include both the portion paid by the employer and the portion paid by the employee. Please see the chart below from the IRS’ webpage and its questions and answers for more information.

The chart below illustrates the types of coverage that employers must report on Form W-2. Certain items are listed as “optional” based on transition relief provided by Notice 2012-9 (restating and clarifying Notice 2011-28). Future guidance may revise reporting requirements but will not be applicable until the tax year beginning at least six months after the date that the IRS issues its guidance.

Form W-2 Reporting of Employer-Sponsored Health Coverage

12/1/2019