Compliance Recap | October 2022

IRS Announces Increased Limits for Certain Employee Benefits, Higher Fines for ACA Reporting Failures

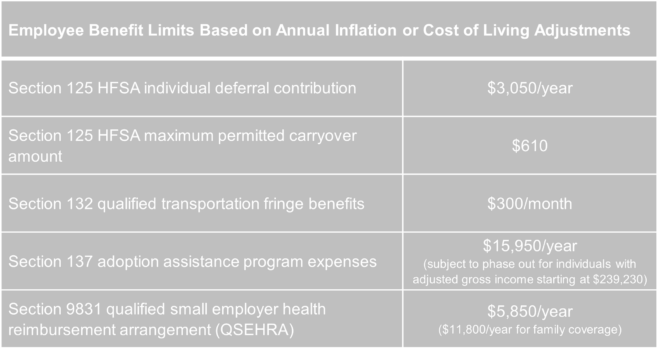

Each year, just as the leaves turn to the fiery shades of autumn, the Internal Revenue Service (IRS) announces how much more “green” will be available during the coming year under various employee benefit programs. The IRS recently released Revenue Procedure 2022-38 in which it has updated many key employee benefit limits based on annual inflation or cost-of-living adjustments. The good news is that recent higher inflation trends have led to the IRS providing for higher-than-typical increases in both the amount that individuals can contribute to a health flexible spending arrangement (HFSA), as well as the amount they can carry over in a plan including that feature.

Effective for tax years beginning in 2023, the following higher limits will apply:

Employers should keep the adjusted limits handy as they prepare for 2023 and communicate with their employees regarding various benefit options.

Additionally, the IRS has announced that employers that fail to file ACA Forms 1095 in 2024 (reporting for 2023) can be subject to a $310 penalty per form. The updated penalty for failure to provide individual statements to employees also will increase to $310 per statement. Since the penalties are cumulative, an employer that fails to provide an employee statement and fails to file with the IRS can be penalized up to $620 for each required form.

As we have noted previously, the IRS continues to be less lenient with late ACA report filers. As fines continue to increase, employers with filing obligations should take great care to ensure that their reporting processes ensure timely filing and timely distribution of individual statements.

Read the full advisor here: IRS Announces Increased Limits for Certain Employee Benefits, Higher Fines for ACA Reporting Failures

ACA Reporting Forms and Draft Instructions Available with Limited Changes for 2022

The Affordable Care Act (ACA) information reporting forms and draft instructions for 2022 are now available.

- Forms 1094-B and 1095-B are filed by minimum essential coverage providers (insurers, government-sponsored programs, and some self-insuring employers and others).

- Forms 1094-C and 1095-C are filed by applicable large employers (ALEs) to provide information that the IRS needs to administer employer shared responsibility penalties and eligibility for premium tax credits.

While there are essentially no changes to the forms, the deadline for furnishing a given year’s Forms 1095-B and 1095-C to individuals has been permanently extend until 30 days after January 31 of the immediately following year. The proposed extension generally aligns with extensions that have been granted for each year since the reporting requirements took effect. Forms 1094-B and 1094-C (transmittals with statements) would be required to be filed with the IRS by February 28, 2023, or March 31, 2023, if filing electronically.

Final Rule Resolves “Family Glitch” for ACA Marketplace Coverage

The Department of the Treasury recently issued final regulations to make the premium tax credit (PTC) for Marketplace health coverage available to more individuals starting in 2023. The new rule changes the IRS’s interpretation of group health coverage affordability for determining PTC eligibility for family members. Whereas the IRS previously only considered the affordability of employer-offered individual health coverage, the new rule looks at the affordability of family coverage to decide whether spouses and dependents can elect Marketplace coverage and receive a PTC. The Biden Administration estimates that the change will result in more than one million individuals qualifying for a PTC for the first time.

Employers should understand, however, that the new rule will not change the affordability and minimum value rules under the Affordable Care Act (ACA) for determining whether an applicable large employer (ALE) must pay an Employer Shared Responsibility Penalty (ESRP). Similarly, the new rule does not alter the information an ALE must report to the IRS annually under the ACA.

Background

The ACA states that individuals who enroll in Marketplace coverage can get a PTC for any month of coverage when they are ineligible for minimum essential coverage (MEC), including employer group coverage. An individual is considered ineligible if MEC is unaffordable or does not provide minimum value.

Currently, employer coverage is unaffordable if the share of the annual premium the employee must pay for self-only coverage is more than 9.61% of household income. That also means coverage is unaffordable for related family members if the employee’s cost for self-only coverage is unaffordable – the employee’s cost for family coverage does not matter.

Additionally, employer coverage does not provide minimum value if the plan’s share of the total allowed cost of benefits provided under individual coverage is less than 60%. As with affordability, the IRS judges minimum value without considering whether employer coverage provides minimum value to an individual’s spouse or dependents. So, a family member could not receive a PTC even if the family coverage they could get through an employer-sponsored plan fails to provide minimum value to them.

Summary of the New Rule

Following a January 2021 Executive Order to review existing regulations, policies, and practices to see if they limit access to financial aid for ACA Marketplace coverage, the Treasury Department and the IRS concluded that their current interpretation of ACA affordability and minimum value requirements disadvantaged thousands of families. Thus, they now state that a more appropriate interpretation of the ACA requires separate affordability and minimum value analysis for employees and family members to resolve the so-called family glitch created by the current interpretation.

The new rule interprets the ACA to base affordability of employer coverage for an employee’s spouse or tax dependents on the cost of covering the employee and their family members. So, for 2023, an eligible employer-sponsored plan will be deemed affordable for related individuals only if an employee’s required contribution for family coverage does not exceed the then-current indexed percentage of an employee’s household income (that is, 9.12% for 2023).

Likewise, the new rule interprets the ACA to require an eligible employer-sponsored plan to ensure a plan provides 60% minimum value coverage to related individuals. Finally, the rule directly states that an eligible employer-sponsored plan provides minimum value to a related individual only if, in addition to covering at least 60% of the total allowed costs of benefits provided to the related individual, the plan benefits include substantial coverage of inpatient hospital services and physician services.

Rule Does Not Apply to ALE Reporting or ESRP

Under the ACA, affordability and minimum value for PTC eligibility is different than for assessing ALE penalties under Code Section 4980H(b). The new rule is likely to create confusion given such similar terms, but it will not alter the affordability calculation or minimum value determination for any reason relating to annual ACA reporting or for assessing shared responsibility penalties. ALEs will not need to adjust any group health plan design, administrative processes or communications regarding affordability and minimum value, including any affordability safe harbor choice under ESRP rules.

Conclusion

Many advocacy groups welcome the final rule and point to the projected increase in the number of individuals who are likely to enroll in the Marketplace and receive a PTC for the first time. However, some observers read the preamble to the rule, especially its detailed statutory analysis, to signal that there could be litigation looming. In either event, the IRS plans to provide educational materials to consumers through healthcare.gov ahead of the upcoming Marketplace enrollment period. Employers should direct individuals to the site for more information.

Read the full advisor here: Final Rule Resolves “Family Glitch” for ACA Marketplace Coverage

December 27 Due Date for Prescription Drug Cost Reporting is Approaching

As part of the Consolidated Appropriations Act of 2021 (CAA), group health plans and carriers will soon be required to report certain demographic and spending information about a plan’s prescription drug expenditures. The Departments will use this data to publish public reports on prescription drug reimbursements, pricing trends, and the impact of prescription drug costs on premium costs. The pharmacy reporting requirement generally applies to group health plans (both fully insured and self-insured) and carriers.

The Centers for Medicare and Medicaid Service (CMS) released several FAQs that clarify requirements under the CAA for prescription drug reporting.

- Which wellness services should I include in the RxDC report? (published 8/25/2022)

- Do the RxDC reporting requirements apply to limited-scope dental or limited-scope vision plans? (published 8/25/2022)

- Will there be training for RxDC? (published 8/25/2022)

- Where can I find the updated RxDC reporting instructions that were published on June 30, 2022? (published 8/25/2022)

- When can I submit my data in the Health Insurance Oversight System (HIOS)? (published 8/25/2022)

- How should I handle vaccines for RxDC reporting purposes? (published 9/1/2022)

- Does a group health plan need a HIOS Issuer ID or a HIOS Plan ID for RxDC Reporting? (published 9/1/2022)

- I am a vendor submitting the RxDC report on behalf of a group health Does the group health plan need to be registered in HIOS? (published 9/1/2022)

- I am a vendor submitting the RxDC report for multiple clients. Can I create multiple submissions in the RxDC HIOS module? (published 9/1/2022)

- May multiple reporting entities submit different data file types (D1 – D8) for the same plan or issuer? (published 9/23/2022)

- When multiple reporting entities submit data files for the same plan or issuer, does each reporting entity need to submit a plan list (P1, P2, and/or P3)? (published 9/23/2022)

- When multiple reporting entities submit data files for the same plan or issuer, does each reporting entity need to fill out every field in the plan list? (published 9/23/2022)

- May multiple reporting entities submit the same data file type for the same plan or issuer? (published 9/23/2022)

- How do I determine the top 50 drugs with the greatest increase in spending in D5 for a client if the client had a different reporting entity in the previous reference year? (revised 10/4/2022)

- How do I calculate restated prior year rebates, fees, and other remuneration in data files D6 – D8 for a client if the client had a different reporting entity in a previous reference year? (published 9/23/2022)

Employer Action Items

Group health plans and carriers are required to submit their first pharmacy report by December 27, 2022 (for calendar years 2020 and 2021) and will need the assistance of their carriers, TPAs, PBMs, or other similar vendors. Fully insured groups should confirm with their carriers that they will comply with this requirement and obtain this in a written document. Self-insured groups should identify and contract with their TPA or PBM to fulfill this requirement on the plan’s behalf.

Question of the Month

- What are the Medicare Part A and Part B enrollment periods?

- You can only sign up for Part B (and/or Part A if you have to buy it) during these enrollment periods.

Initial Enrollment Period

You can first sign up for Part A and/or Part B during the 7-month period that begins 3 months before the month you turn 65, includes the month you turn 65, and ends 3 months after the month you turn 65.

If you sign up for Part A and/or Part B during the first 3 months of your Initial Enrollment Period, in most cases, your coverage begins the first day of your birthday month. However, if your birthday is on the first day of the month, your coverage starts the first day of the prior month.

If you sign up and are paying for Part A and/or Part B the month you turn 65 or during the last 3 months of your Initial Enrollment Period, the start date for your Part B coverage will be delayed (in 2022).

Beginning January 1, 2023, if you sign up the month you turn 65 or during the last 3 months of your Initial Enrollment Period, your coverage starts the first day of the month after you sign up.

Special Enrollment Period

After your Initial Enrollment Period is over, you may have a chance to sign up for Medicare during a Special Enrollment Period. For example, if you didn’t sign up for Part B (or Part A if you have to buy it) when you were first eligible because you have group health plan coverage based on current employment (your own, a spouse’s, or a family member’s if you have a disability), you can sign up for Part A and/or Part B:

- Anytime you’re still covered by the group health plan.

- During the 8-month period that begins the month after the employment ends or the coverage ends, whichever happens first.

Usually, you won’t have to pay a late enrollment penalty if you sign up during a Special Enrollment Period. This period doesn’t apply if you’re eligible for Medicare based on End-Stage Renal Disease (ESRD), or you’re still in your Initial Enrollment Period.

COBRA (Consolidated Omnibus Budget Reconciliation Act) coverage, retiree health plans, VA coverage, and individual health insurance coverage (like coverage through the Health Insurance Marketplace) aren’t considered coverage based on current employment.

There are other circumstances where you may be able to sign up for Medicare during a Special Enrollment Period. Beginning January 1, 2023, you may be eligible for a Special Enrollment Period if you miss an enrollment period because of certain exceptional circumstances, like being impacted by a natural disaster or an emergency, incarceration, or losing Medicaid coverage.

General Enrollment Period

If you have to pay for Part A but don’t sign up for it or don’t sign up for Part B (for which you must pay premiums) during your Initial Enrollment Period, and you don’t qualify for a Special Enrollment Period, you can sign up during the General Enrollment Period from January 1 to March 31 each year. You may have to pay a higher Part A and/or Part B premium for late enrollment.

Beginning January 1, 2023, when you sign up during this period, your coverage starts the first day of the month after you sign up.