Compliance Recap | October 2024

October brought the second of two Centers for Medicare & Medicaid (CMS) Medicare Part D annual disclosures, in the form of Creditable Coverage Letters. The IRS released the 2025 cost-of-living adjustment information affecting employee benefit plans. We were reminded that while there are no federal requirements for time off to vote, many states mandate it. Employers sponsoring an individual coverage HRA (ICHRA) should have provided their annual notice to plan participants. An FAQ was released providing guidance on the requirements of the Women’s Health and Cancer Rights Act. As open enrollment begins for many employers, remember important tips to remain compliant.

Medicare Part D Creditable Coverage Notices

Group health plans that provide prescription drug coverage to Medicare Part D eligible individuals must disclose whether that coverage is creditable or not creditable before the start of the annual coordinated election period for Medicare Part D. Creditable coverage means that the coverage is expected to pay on average as much as the standard Medicare prescription drug coverage. Model disclosure notices are available on the Centers for Medicare & Medicaid Services (CMS) website.

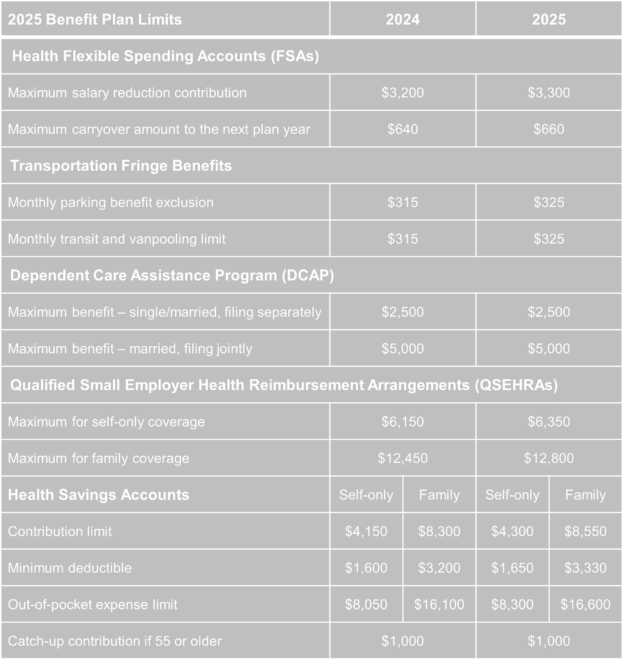

IRS Releases 2025 Benefit Plan Limits

Recent IRS cost-of-living adjustments will affect key benefit programs for 2025. Understanding and implementing these changes can help optimize tax advantages, maintain compliance, and support employees in managing their healthcare and other related costs.

Employer Considerations

- Update all benefits documents to reflect 2025 limits.

- Work with payroll and benefits vendors to implement new contribution and reimbursement caps.

- Communicate the 2025 limits to employees during open enrollment, highlighting potential impacts.

- Brief HR teams on new limits to ensure accurate administration and employee support.

Time Off for Voting

Federal law doesn’t mandate time off for voting, but 30 states and local governments require it, especially when work hours limit voting availability.

Regulations vary on whether voting leave is paid or unpaid and on the amount of time provided. Some laws also dictate when employees can take this leave and may require employers to post voting rights information.

Employer Considerations

In areas without voting-leave laws, it’s best practice to offer paid time if needed or consider other ways to support voting, like offering information on early voting.

Emerging issues include handling requests during early voting periods or for employees living in a different state. Experts advise following the law most beneficial to the employee, in the spirit of encouraging voting.

ICHRA Notice to Plan Participants

Employers that offer an Individual Coverage Health Reimbursement Arrangement (ICHRA) calendar year plan must furnish written notice to each participant containing specific information about the ICHRA 90 days before the beginning of the plan year. The U.S. Department of Labor (DOL) provides a model notice.

IRS Releases FAQs on Women’s Health and Cancer Rights Act

On October 21, 2024, new FAQs on the Affordable Care Act (ACA) and the Women’s Health and Cancer Rights Act (WHCRA) were released, offering important guidance for group health plans related to breast reconstruction following a mastectomy.

The WHCRA mandates that group health plans covering mastectomies must also include coverage for breast reconstruction, symmetry surgery on the opposite breast, prostheses, treatment of complications like lymphedema, and aesthetic flat closure, if chosen by the patient. This coverage must be coordinated between the patient and their attending physician. Sponsors of self-funded, non-federal government plans may opt out of WHCRA requirements.

Employer Considerations

Affected employers should:

- Ensure that these new guidelines are integrated into company health plans to maintain compliant healthcare coverage for employees.

- Educate employees on their rights under WHCRA to ensure they’re informed about their coverage options, emphasizing the role of physician-patient consultation in determining appropriate treatments, and regularly reviewing group health plans to confirm WHCRA compliance.

Open Enrollment Compliance

Open enrollment season highlights the intricate rules that govern employer-sponsored health and welfare plans. As you prepare to announce benefit options for the upcoming year, address employee questions, and manage the administrative details, it’s essential to keep important legal requirements in mind.

COBRA compliance requires notifying employees who lose benefits due to termination of employment that they have the opportunity to continue coverage. Individuals enrolled in COBRA must be notified of open enrollment. Automating notifications and using checklists can help avoid costly penalties.

Similarly, HIPAA mandates the protection of employee data, especially during open enrollment. Ensure secure data handling, train staff on privacy rules, and verify that third-party vendors follow strict data protocols to protect sensitive information.

Incomplete or outdated Summary Plan Descriptions (SPDs) and Summary of Benefits and Coverage (SBCs) are common compliance issues. Under ERISA, these documents must accurately outline benefits and failing to distribute updated versions risks penalties. Review and update SPDs and SBCs annually and ensure timely distribution. Digital access to current documents can help employees stay informed and prevent compliance issues.

Documenting employee benefit elections is essential to prevent disputes and meet ACA compliance requirements. Digital systems can track and confirm employee choices, creating a clear audit trail. Additionally, regular benefits audits are crucial to ensure accurate contributions, eligibility, and regulatory compliance. Proactive reviews help identify and address compliance issues before they escalate, keeping your benefits program running smoothly.

Question of the Month

- How long should an employer keep insurance benefits proposals and quotes?

- ERISA has a six-year statute of limitations. Therefore, it’s prudent to keep insurance quotes and proposals for at least six years to justify decisions made by the company within ERISA’s statute of limitations.